Categories

Home Buying TipsPublished October 24, 2025

"Buying Starbucks” Isn’t the Problem: Here’s What Actually Might Help

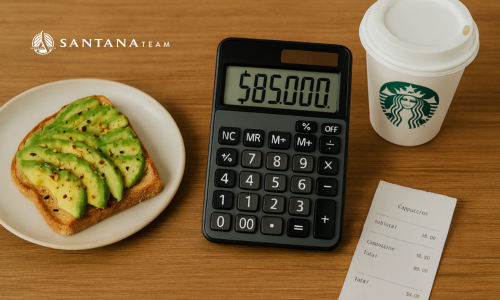

I just read another article saying that if Millennials and Gen Z would just stop buying Starbucks, we could all afford houses. Sure, because obviously a $6 latte is the only thing keeping us from buying a $700,000 home in Boston.

Let’s look at the math instead of the moralizing. To buy that $700,000 home, even with a 10% down payment and typical closing costs, you’d need roughly $85,000–$90,000 in cash up front. If you saved $15 a day in “Starbucks money,” it would take about 15 years to get there...and by then, that same home could easily cost more than $1 million. So no, it’s not the coffee. It’s the cost of housing, wages, and a system that hasn’t kept up.

1. Get Your Financial Footing

This part isn’t glamorous, but it matters. Before assuming homeownership is out of reach forever, take control of what you can.

- Know your numbers. Track what you earn, where it goes, and what’s left to save. It’s not fun, but it’s freeing.

- Question every recurring charge. Is that razor subscription really saving you money? Do you need four streaming services? Those quiet little charges add up faster than you think.

- Cut what you can, not what makes life livable. You don’t have to swear off dinners with friends or cancel every trip, just set real limits and stick to them.

- Learn the basics of credit scores, debt ratios, and compound interest. These are the gatekeepers for mortgage approval.

- Meet with a reputable, fiduciary financial advisor. The goal isn’t judgment, it’s strategy. A good one can help you understand your timeline and the steps to make it real.

Getting your financial house in order doesn’t guarantee a literal house, but it puts you in position when the opportunity shows up.

2. Redefine What “Buying a Home” Looks Like

Your parents might’ve bought their dream home first. Ours will probably buy their dream home second or third. Your first place is your on-ramp. The key is to get into the market so you can stop paying your landlord’s mortgage and start paying your own.

- Start smaller or farther out. A condo in Medford or Woburn might build the equity that someday buys a single-family in Cambridge.

- House hack. Rent a room or unit to offset your mortgage.

- Co-buy with friends or family. Write the legal agreements early and be clear about exits. Equity beats rent every time.

- Use first-time buyer programs. Massachusetts has down payment assistance and low-rate options that can bridge the gap faster than years of saving alone.

- Talk to a lender early. Even if you’re a year out, you’ll learn what needs fixing (credit, debt ratio, income) before you start shopping.

It’s not about perfection. It’s about progress and positioning yourself where equity can finally start working for you.

3. Push for Bigger Fixes

Let’s be honest: no one can budget their way out of a broken housing system. Personal responsibility matters, but it can’t replace collective change.

- Build more housing. Massachusetts consistently under-produces homes. We need zoning reform, faster permitting, and more multi-family construction near transit.

- Encourage starter homes and condos. Developers build luxury because that’s where the profit is. Policy can shift those incentives.

- Ease student debt pressure. Wages haven’t matched tuition, and debt-to-income ratios keep young adults locked out of mortgages.

- Modernize tax incentives. Reward first-time buyers and long-term stability instead of speculation and flipping.

None of this happens overnight, but the conversation has to shift from blaming avocado toast to demanding systemic reform while still taking smart personal steps.

The Bottom Line

Buying a home today takes strategy, sacrifice, and support, not shame. Skip a few subscriptions if it helps, sure. But don’t believe anyone who says a cup of coffee stands between you and the keys to a house. The real fix is part personal discipline, part collective action, and a lot of persistence.

Thinking about buying your first home in Greater Boston? Our team helps first-time buyers navigate financing, down-payment programs, and neighborhoods that fit both your budget and lifestyle. Connect with Victoria Goodman to start your home-ownership plan today.

Market conditions and program details change over time. Data current as of October 2025.

|

or another way